Disclosure: I have no positions in any stocks mentioned, but may initiate a long position in HK over the next 72 hours.

Ever since the old Petrohawk management team purchased Ram Energy and invested millions of dollars last December, analysts have suggested buying the new Halcon Resources Corporation (HK). Unfortunately, unless investors bought during the first two days, anybody holding now is under water. In essence, any investors buying the stock this year have lost money.

The domestic land E&P firm is building positions in leading unconventional shale plays, such as the Eagle Ford, Bakken, Utica, and the Tuscaloosa Marine. Investors now though get the option of following those insiders who made significant purchases in the $5 area last week. Oddly though, after a strong surge Tuesday on the news of the insider purchases, the stock has started sinking again. Should investors jump in with the insiders or dump the stock?

Deals

One of the biggest initial concerns was investing in a company that planned several transformational deals in order to build up reserves and drilling locations. Investors clearly knew the past of CEO Floyd Wilson, former CEO of Petrohawk, but it was unclear what dilutive impacts of any significant deals would have on shareholders who rushed into the stock.

The company has purchased GeoResources, East Texas Assets, and Petro-Hunt to build up the acres in the shale plays. All of these assets transformed the company from acquirer to a driller. In the process, the company has gone from a 4,000 Boe/d conventional driller to a forecast of averaging over 40,000+ Boe/d in 2013. The question is whether the stock has kept up with this drilling potential.

Q3 2012 Highlights

The company reported the following highlights for Q3 2012:

- Net production for the third quarter increased to an average of 11,185 barrels of oil equivalent per day (Boe/d), of which 77% was oil and natural gas liquids (NGLs), compared to 3,924 Boe/d for the same period of 2011.

- Revenues for the three months ended Sept. 30, 2012, increased to $73.1 million, compared to $24.2 million for the three months ended Sept. 30, 2011, largely due to increased production volumes related to the GeoResources and East Texas Assets acquisitions.

- Reported a net loss for the quarter of $0.9 million, or $0.01 per diluted share, after adjusting for selected items (primarily related to the non-cash impact of derivatives and acquisition and merger transaction costs), compared to a net loss of $2.6 million, or $0.10 per diluted share in the comparable quarter of 2011.

- Cash flow from operations before changes in working capital was $29.2 million for the quarter, or $0.15 per diluted share, compared to $9.4 million, or $0.36 per diluted share for the same period of 2011.

These earnings aren't that meaningful considering they only encapsulate a portion of the recent deals, nor does it include some of the expected drilling increases from the purchased assets. The quarterly revenue should more than quadruple next year.

Valuation

The company has a very compelling valuation after this year's 50% drop in the stock price. Steve Zachritz's article "Halcon Resources Bigger, Oiler, And Still Cheaper Than You Think" provides a great analysis of the pro forma EBITDA possibilities of the transformed Halcon.

One noteworthy number is the revenue estimates that easily surpass those of analysts. Steve provides a midpoint of nearly $1.18 billion while the highest analyst estimate is just over $1.16 billion. Based on his firm's EBITDA estimates, it is no wonder the insiders chose these stock levels to purchase the stock.

Stock Price

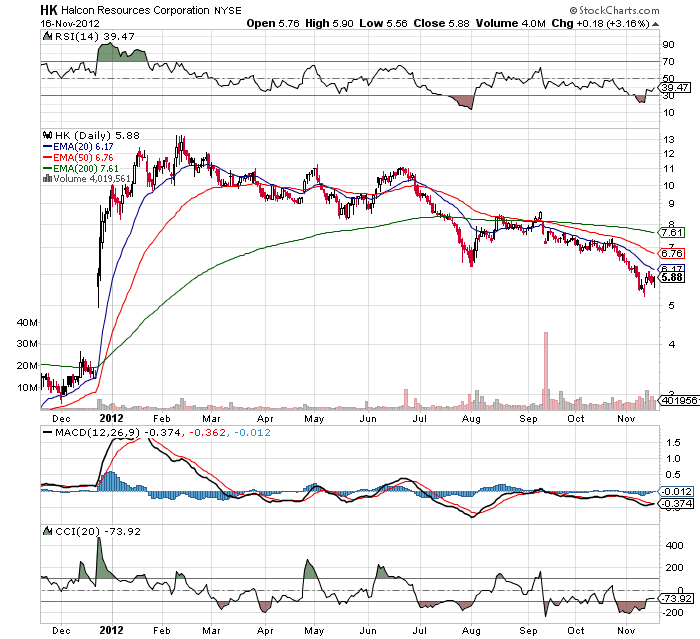

As mentioned earlier, the stock has been in a major slide since peaking back over $13 in February. Though the company continues to execute on the transformational plan, investors continue fleeing the stock.

One-Year Chart -- Halcon Resources

Click to enlarge image.

Conclusion

Based on the tremendous track record of Floyd Wilson and the other management team at Halcon, investors originally sent this stock soaring with the re-entry back into the oil exploration industry. Now investors get the opportunity to jump back into the stock after the excitement has cooled and the market has lost interest. Not to mention that those same insiders just signaled the extreme value proposition now offered.

The detractors will suggest that the insider purchases were only an immaterial $1.5 million. Though accurate, investing alongside the purchase price of a management team still beats the alternative