Eclipse has been working with mineral owners to amend the leases, converting the full five-year extension option into annual "delay rental" extensions

http://seekingalpha.com/article/3777466-eclipse-resources-a-tough-y...

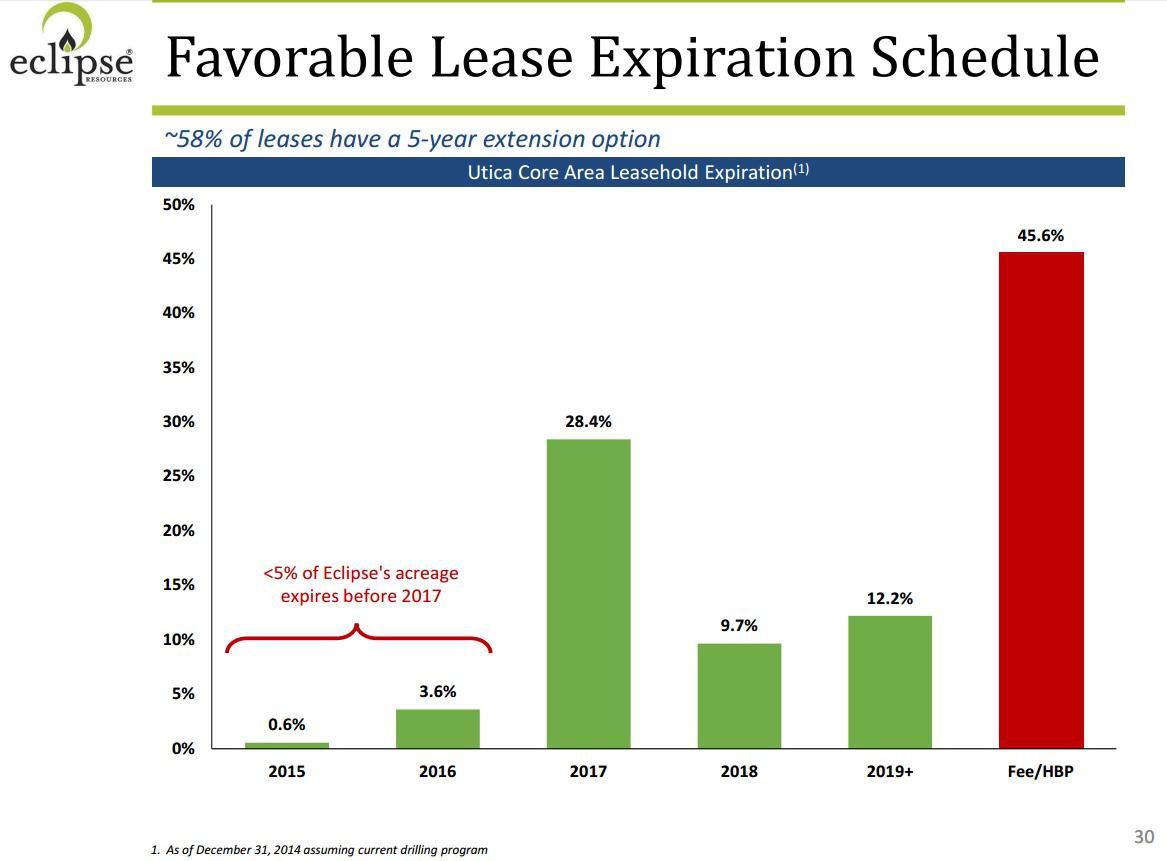

Eclipse is facing significant lease expirations in 2017. Roughly 26,000 acres will be up for renewal in 2017, assuming none of it is drilled next year. The vast majority of that acreage is in the dry gas window, according to the company (a large percentage of the company's liquids-rich acreage is already held by production, either from Utica wells or conventional wells).

The majority of the leases that expire in the future have extension options, with an average cost of roughly $5,000 per acre, according to the company. Eclipse has been working with mineral owners to amend the leases, converting the full five-year extension option into annual "delay rental" extensions. The company commented that it received positive responses with regard to approximately 15% of its leases from the owners in less than two months.

While the response rate is encouraging, it is clear that lease renewal costs will be a significant capital item for the company in the next few years. Assuming 50% of all leases expiring in 2017 are converted to delay rental payments and half of the remaining expiring leases are renewed at $5,000 per acre, Eclipse's land-related spending in 2017 may exceed $50 million, which would be a very significant cash outlay, given the company's tight liquidity situation.

(click to enlarge)

(Source: Eclipse Resources, December 2015)

Views: 752

Replies to This Discussion

-

Permalink Reply by searcherone on

-

Since this process has been going on since mid September and the article is written in late December, IMHO doesn't seem 15% is a high percentage of landowners who have signed the amendment.

-

Permalink Reply by Philip Brutz on

-

Could someone post the wording of the "delay rental" extension?

-

Permalink Reply by Philip Brutz on

-

http://www.businesswire.com/news/home/20160104006469/en/

Eclipse Resources Fourth Quarter 2015 Operational Update and Conference Participation

STATE COLLEGE, Pa.--(BUSINESS WIRE)--Eclipse Resources Corporation (NYSE:ECR) (the “Company”) today is pleased to provide an operational update, its initial outlook on the First Quarter 2016 guidance and capital budget and the participation of members from the Company’s executive management team in the following upcoming investor conferences:

- Wednesday January 6, 2016 through Thursday January 7, 2016 (Miami, FL)- Goldman Sachs Global Energy Conference. Benjamin W. Hulburt (Chairman, President and CEO) and Matthew R. DeNezza (Executive Vice President and CFO) will host one-on-one meetings.

- Thursday January 13, 2016 (Boston, MA)- BMO Capital Markets Energy Forum. Benjamin W. Hulburt (Chairman, President and CEO) and Matthew R. DeNezza (Executive Vice President and CFO) will host one-on-one meetings.

The Company has posted an updated corporate presentation on the Company website at www.eclipseresources.comwhich includes information contained in this release as well as additional updated information.

Operational Update

The Company continues to closely monitor the commodity price environment, and the Company currently plans to minimize its drilling and completion activity until commodity prices improve. Despite its drilling cessation, which the Company initiated in November of 2015, the Company believes it is on pace to exceed the high end of its fourth quarter 2015 and full year production guidance range. Based on preliminary estimates, which are subject to change as final sales figures are determined, the Company currently anticipates that it exited 2015 with approximately 268 MMcfe per day of net production with fourth quarter 2015 average net production of at least 236 MMcfe per day, and full year 2015 average net production of approximately 206 MMcfe per day. Additionally, the Company estimates that it exited the year with $281 million in liquidity derived from its undrawn revolving credit facility and cash on hand of approximately $184 million.

The Company is pleased to announce that it placed all seven of its Fuchs/Dietrich wells in the Utica Shale Dry Gas East area into sales during the fourth quarter of 2015. These seven wells were drilled with lateral lengths ranging from approximately 7,450 feet to 10,520 feet (average lateral length of approximately 8,800 feet) and were completed using what the Company currently believes to be an “optimized” frack design. The wells have been placed into sales and were produced at the Company’s Type Well target rate with initial casing pressures of 7,500-8,000 psi.

Given the lower current market prices for both natural gas and oil, coupled with the uncertain outlook in the near term, the Company is focusing its initial 2016 plan on limiting cash outlays on drilling while allowing for greater productivity as prices rebound. To implement this strategy, the Company has begun voluntarily reducing its aggregate operated production to attempt to maintain net production at approximately the same level as its 2015 average, or approximately 200 MMcfe per day, until commodity prices recover. As the Company has both liquids/condensate rich and dry natural gas production areas currently producing the Company plans to adjust its production mix according to changes in the commodity prices for the near term. The Company believes these measures are prudent given the significant decline in oil and natural gas prices as they will enable the Company to maintain sufficient cash flows to meet its obligations, limit use of cash on hand for drilling expenses, avoid selling its valuable products in a depressed price environment and return to its historic production growth profile as commodities begin to rebound in the future.

For the first quarter 2016, the Company anticipates capital expenditures of approximately $33 million, which will include the drilling and completion of 1 net, extended reach well along with associated land and non-operated activity that was commenced in the fourth quarter of 2015. The Company will focus on managing production based upon wells that demonstrate the best variable margin in the current commodity price environment. The table below outlines Eclipse Resources’ first quarter 2016 guidance along with the previously announced fourth quarter and full year 2015 guidance.

Q4 2015 FY 2015 Q1 2016 Production Mmcfe/d 225 ‐ 235 202 ‐ 205 ~200 % Gas 68% ‐ 74% 64% ‐ 66% 73%-80% % NGL 16% ‐ 18% 18% ‐ 20% 15%-17% % Oil 10% ‐ 14% 15% ‐ 17% 6%-10% Gas Price Differential1 $(0.12) ‐ $(0.22) $(0.12) ‐ $(0.15) $(0.10) - $(0.20) FT Expense

$(0.38) ‐ $(0.49)

$(0.30) ‐ $(0.34)

$(0.40) - $(0.50) Gas Price Differential with FT expense1

$(0.50) ‐ $(0.71) $(0.42) ‐ $(0.49) $(0.50) - $(0.70) Oil Differential1 $(11.00) ‐ $(13.00) $(11.25) ‐ $(12.25) $(11.25) - $(12.25) NGL % WTI 15% ‐ 25% 20% ‐ 24% 20% -30% Operating Expenses ($/Mcfe)2 $1.32 ‐ $1.37 $1.28 ‐ $1.33 $1.35 -$1.45 Cash G&A ($mm)3 $10 ‐ $12 $45 ‐ $47 $11 - $12 CAPEX ($mm)4,5 $330 $33 1. Excludes impact of hedges 2. Excludes firm transportation, DD&A, exploration, and general and administrative expenses 3. Excludes costs associated with rig terminations 4. Includes routine lease acquisition, land related expenses, and net of projected midstream reimbursements; excludes land and producing asset acquisitions

5. Includes delay rental payments which are classified as exploration for financial reporting purposes Commenting on the Company’s operations, Benjamin Hulburt, Chairman, President and CEO said, “As natural gas prices hover around fifteen year lows, I believe we are making the financially prudent decision regarding our significantly decreased capital spending plan and the curtailment of our production. Although we are not setting a capital budget for the year at this time, we currently anticipate that our ultimate capital plan, absent a significant increase in commodity prices, will be constructed with the objective of ending 2016 with a cash balance and no new debt drawn. As well, this plan will allow the Company flexibility to adjust which wells are curtailed throughout the year based on operating costs, volume commitments and commodity prices.”

-

Permalink Reply by searcherone on

-

Would anyone like to comment on the slides in Eclipse's slides about "Aggressive Pressure Management" which Eclipse says produces 35% more before the initial decline begins.

My opinion two issues affecting Eclipse which are not reflected in the presentation are: the outcome of the Ohio Supreme Court Case of Hupp vs. Beck Energy.XTO as well as the Bureau of Land Management decision about weather to drill the Wayne National Forest. Eclipse has much acreage bordering Wayne National Forest as well as acreage held by Beck/XTO.

Top Content

Latest Activity

- Top News

- Everything

Jeff replied to Petroleum Attorney 1976's discussion 'FYI- Mineral Owners in the State of Ohio (Utica Shale area's)'

© 2026 Created by Keith Mauck (Site Publisher).

Powered by

![]()